![]()

The FastJM package implement efficient computation of

semi-parametric joint model of longitudinal and competing risks

data.

The FastJM package comes with several simulated

datasets. To fit a joint model, we use jmcs function.

require(FastJM)

#> Loading required package: FastJM

#> Loading required package: MASS

#> Loading required package: statmod

data(ydata)

data(cdata)

fit <- jmcs(ydata = ydata, cdata = cdata,

long.formula = response ~ time + gender + x1 + race,

surv.formula = Surv(surv, failure_type) ~ x1 + gender + x2 + race,

random = ~ time| ID)

fit

#>

#> Call:

#> jmcs(ydata = ydata, cdata = cdata, long.formula = response ~ time + gender + x1 + race, random = ~time | ID, surv.formula = Surv(surv, failure_type) ~ x1 + gender + x2 + race)

#>

#> Data Summary:

#> Number of observations: 3067

#> Number of groups: 1000

#>

#> Proportion of competing risks:

#> Risk 1 : 34.9 %

#> Risk 2 : 29.8 %

#>

#> Numerical intergration:

#> Method: pseudo-adaptive Guass-Hermite quadrature

#> Number of quadrature points: 6

#>

#> Model Type: joint modeling of longitudinal continuous and competing risks data

#>

#> Model summary:

#> Longitudinal process: linear mixed effects model

#> Event process: cause-specific Cox proportional hazard model with non-parametric baseline hazard

#>

#> Loglikelihood: -8989.389

#>

#> Fixed effects in the longitudinal sub-model: response ~ time + gender + x1 + race

#>

#> Estimate SE Z value p-val

#> (Intercept) 2.01853 0.05704 35.38803 0.0000

#> time 0.98292 0.03147 31.22885 0.0000

#> genderMale -0.07766 0.05860 -1.32527 0.1851

#> x1 -1.47810 0.05851 -25.26356 0.0000

#> raceWhite 0.04527 0.05911 0.76581 0.4438

#>

#> Estimate SE Z value p-val

#> sigma^2 0.49182 0.01793 27.43751 0.0000

#>

#> Fixed effects in the survival sub-model: Surv(surv, failure_type) ~ x1 + gender + x2 + race

#>

#> Estimate SE Z value p-val

#> x1_1 0.54672 0.18540 2.94892 0.0032

#> genderMale_1 -0.18781 0.11935 -1.57359 0.1156

#> x2_1 -1.10450 0.12731 -8.67602 0.0000

#> raceWhite_1 -0.10027 0.11802 -0.84960 0.3955

#> x1_2 0.62986 0.20064 3.13927 0.0017

#> genderMale_2 0.10834 0.13065 0.82926 0.4070

#> x2_2 -1.76738 0.15245 -11.59296 0.0000

#> raceWhite_2 0.03194 0.13049 0.24479 0.8066

#>

#> Association parameters:

#> Estimate SE Z value p-val

#> (Intercept)_1 0.93973 0.12160 7.72809 0.0000

#> time_1 0.31691 0.19318 1.64051 0.1009

#> (Intercept)_2 0.96486 0.13646 7.07090 0.0000

#> time_2 0.03772 0.24137 0.15629 0.8758

#>

#>

#> Random effects:

#> Formula: ~time | ID

#> Estimate SE Z value p-val

#> (Intercept) 0.52981 0.03933 13.47048 0.0000

#> time 0.25885 0.02262 11.44217 0.0000

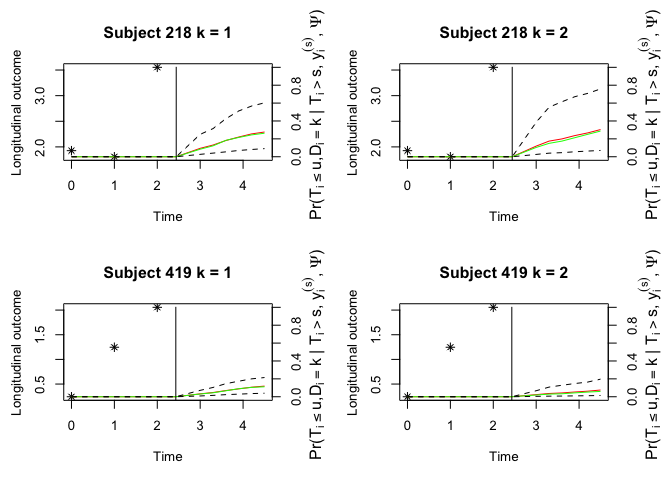

#> (Intercept):time -0.02765 0.02529 -1.09330 0.2743The FastJM package can make dynamic prediction given the

longitudinal history information. Below is a toy example for competing

risks data. Conditional cumulative incidence probabilities for each

failure will be presented.

ND <- ydata[ydata$ID %in% c(419, 218), ]

ID <- unique(ND$ID)

NDc <- cdata[cdata$ID %in% ID, ]

survfit <- survfitjmcs(fit,

ynewdata = ND,

cnewdata = NDc,

u = seq(3, 4.5, by = 0.3),

M = 50,

seed = 100)

#> | | | 0% | |= | 2% | |=== | 4% | |==== | 6% | |====== | 8% | |======= | 10% | |========= | 12% | |========== | 14% | |=========== | 16% | |============= | 18% | |============== | 20% | |================ | 22% | |================= | 24% | |=================== | 27% | |==================== | 29% | |===================== | 31% | |======================= | 33% | |======================== | 35% | |========================== | 37% | |=========================== | 39% | |============================= | 41% | |============================== | 43% | |=============================== | 45% | |================================= | 47% | |================================== | 49% | |==================================== | 51% | |===================================== | 53% | |======================================= | 55% | |======================================== | 57% | |========================================= | 59% | |=========================================== | 61% | |============================================ | 63% | |============================================== | 65% | |=============================================== | 67% | |================================================= | 69% | |================================================== | 71% | |=================================================== | 73% | |===================================================== | 76% | |====================================================== | 78% | |======================================================== | 80% | |========================================================= | 82% | |=========================================================== | 84% | |============================================================ | 86% | |============================================================= | 88% | |=============================================================== | 90% | |================================================================ | 92% | |================================================================== | 94% | |=================================================================== | 96% | |===================================================================== | 98% | |======================================================================| 100%

survfit

#>

#> Prediction of Conditional Probabilities of Event

#> based on 50 Monte Carlo samples

#>

#> $`218`

#> $`218`$`Cumulative incidence probabilities for type 1 failure`

#> times Mean Median 95%HDLower 95%HDUpper

#> 1 2.441634 0.00000000 0.00000000 0.00000000 0.0000000

#> 2 3.000000 0.09409995 0.08439099 0.02680045 0.2505176

#> 3 3.300000 0.13096812 0.12189837 0.04061000 0.3148925

#> 4 3.600000 0.18169006 0.18341437 0.05473491 0.4257421

#> 5 3.900000 0.22059759 0.21583291 0.07014845 0.5123262

#> 6 4.200000 0.25554959 0.24445482 0.08128623 0.5671258

#> 7 4.500000 0.27644079 0.26324625 0.09083009 0.6027723

#>

#> $`218`$`Cumulative incidence probabilities for type 2 failure`

#> times Mean Median 95%HDLower 95%HDUpper

#> 1 2.441634 0.0000000 0.0000000 0.00000000 0.0000000

#> 2 3.000000 0.1188501 0.1040518 0.02608558 0.3853528

#> 3 3.300000 0.1748083 0.1497234 0.04007024 0.5540829

#> 4 3.600000 0.1994586 0.1749631 0.04563150 0.6148572

#> 5 3.900000 0.2364823 0.2127958 0.05561986 0.6712990

#> 6 4.200000 0.2665352 0.2506279 0.06341423 0.7084854

#> 7 4.500000 0.3038783 0.2869893 0.07048539 0.7581722

#>

#>

#> $`419`

#> $`419`$`Cumulative incidence probabilities for type 1 failure`

#> times Mean Median 95%HDLower 95%HDUpper

#> 1 2.432155 0.00000000 0.00000000 0.000000000 0.00000000

#> 2 3.000000 0.03253085 0.03069550 0.008767364 0.07148498

#> 3 3.300000 0.04748489 0.04426280 0.015251152 0.10394147

#> 4 3.600000 0.06941185 0.06670128 0.023630057 0.14636707

#> 5 3.900000 0.08820968 0.08998766 0.029119034 0.17407396

#> 6 4.200000 0.10667737 0.10464168 0.035382172 0.20011320

#> 7 4.500000 0.11903075 0.11171259 0.039342101 0.21482290

#>

#> $`419`$`Cumulative incidence probabilities for type 2 failure`

#> times Mean Median 95%HDLower 95%HDUpper

#> 1 2.432155 0.00000000 0.00000000 0.000000000 0.00000000

#> 2 3.000000 0.02360106 0.01955522 0.004430992 0.06728198

#> 3 3.300000 0.03651387 0.02940210 0.006585600 0.10774710

#> 4 3.600000 0.04266639 0.03329662 0.007747423 0.12837243

#> 5 3.900000 0.05312238 0.04334585 0.009734476 0.14772235

#> 6 4.200000 0.06215204 0.05221544 0.011553611 0.16409921

#> 7 4.500000 0.07516719 0.05978386 0.014209057 0.19666594Plot the cumulative incidence function for each failure with the historical longitudinal observations.

oldpar <- par(mfrow = c(2, 2), mar = c(5, 4, 4, 4))

plot(survfit, estimator = "both", include.y = TRUE)

par(oldpar)