PDtoolkit provides collection of tools for probability

of default (PD) rating model development and validation. Keeping in

mind the fact that model development is highly iterative and repetitive

process, having standardized and automated tools for this purpose is of

the utmost importance for analysts. The main goal of this package is to

cover the most common steps of PD model development. As additional

contribution we attempted to add some functionalities which at the

moment of the package development were not presented in R

package ecosystem in area of credit risk modeling. The package available

functionalities are those that refer to univariate, bivariate,

multivariate analysis, calibration and validation. Along with

accompanied monobin and monobinShiny packages,

PDtoolkit provides functions which are suitable for

different data transformation and modeling tasks such as: imputations,

monotonic binning of numeric risk factors, binning of categorical risk

factors, weights of evidence (WoE) and information value (IV)

calculations, WoE coding (replacement of risk factors’ modalities with

WoE values), risk factor clustering, area under curve (AUC) calculation

and others. Beside mentioned features, package provides set of

validation functions for testing homogeneity, heterogeneity,

discriminatory and predictive power of the model.

The following case study shows the usage of PDtoolkit

package. The study is based on publicly available German credit data set

which is available and downloaded from this link, but also

distributed along with PDtoolkit package under the data

frame loans. Presented examples are simplified, but yet

realistic, version of the PD model development and validation. In the

first row, simplification is assumed in final model selection, master

scale creation, calibration and some validation steps, whereas in

practice we usually have highly iterative process with couple of

available options. Anyhow, this does not diminish the practical value of

the presented examples. So, let’s start with a concrete case study.

First, we will import the libraries needed for the following examples.

library(PDtoolkit)

library(monobin)

library(rpart)If the packages are not already installed, run the following code

before the library import

install.packages(c("PDtoolkit", "monobin", "rpart")) in

order to install it from the CRAN, while

devtools::install_github("andrija-djurovic/PDtoolkit") to

install development version.

Then, let’s import and inspect the structure of the modeling data set

- loans.

data(loans)

str(loans)## 'data.frame': 1000 obs. of 21 variables:

## $ Creditability : num 0 0 0 0 0 0 0 0 0 0 ...

## $ Account Balance : chr "1" "1" "2" "1" ...

## $ Duration of Credit (month) : num 18 9 12 12 12 10 8 6 18 24 ...

## $ Payment Status of Previous Credit: chr "4" "4" "2" "4" ...

## $ Purpose : chr "2" "0" "9" "0" ...

## $ Credit Amount : num 1049 2799 841 2122 2171 ...

## $ Value Savings/Stocks : chr "1" "1" "2" "1" ...

## $ Length of current employment : chr "2" "3" "4" "3" ...

## $ Instalment per cent : chr "4" "2" "2" "3" ...

## $ Sex & Marital Status : chr "2" "3" "2" "3" ...

## $ Guarantors : chr "1" "1" "1" "1" ...

## $ Duration in Current address : chr "4" "2" "4" "2" ...

## $ Most valuable available asset : chr "2" "1" "1" "1" ...

## $ Age (years) : num 21 36 23 39 38 48 39 40 65 23 ...

## $ Concurrent Credits : chr "3" "3" "3" "3" ...

## $ Type of apartment : chr "1" "1" "1" "1" ...

## $ No of Credits at this Bank : chr "1" "2" "1" "2" ...

## $ Occupation : chr "3" "3" "2" "2" ...

## $ No of dependents : chr "1" "2" "1" "2" ...

## $ Telephone : chr "1" "1" "1" "1" ...

## $ Foreign Worker : chr "1" "1" "1" "2" ...Note that variable (column) names have some special characters which

is not usually considered as good practice in real studies, but for this

example we will use it as provided originally in data source.

Additionally, in order to present all functionalities of the

PDtoolkit package, we will slightly modify modeling data

set inserting some missing values for certain variables as given

below:

loans$"Credit Amount"[1:10] <- NA

loans$"Age (years)"[30:50] <- NA

loans$"Purpose"[800:820] <- NAUsually the first step in model development is the univariate

analysis. For this purpose we will use univariate function

from the PDtoolkit package:

univariate(db = loans)## rf rf.type bin.type bin cnt pct cnt.unique min p1

## 1 Creditability numeric complete cases complete cases 1000 1.000 2 0 0.00

## 2 Account Balance character complete cases complete cases 1000 1.000 4 NA NA

## 3 Duration of Credit (month) numeric complete cases complete cases 1000 1.000 33 4 6.00

## 4 Payment Status of Previous Credit character complete cases complete cases 1000 1.000 5 NA NA

## 5 Purpose character special cases special cases 21 0.021 1 NA NA

## 6 Purpose character complete cases complete cases 979 0.979 10 NA NA

## 7 Credit Amount numeric special cases special cases 10 0.010 1 Inf NA

## 8 Credit Amount numeric complete cases complete cases 990 0.990 915 250 424.13

## 9 Value Savings/Stocks character complete cases complete cases 1000 1.000 5 NA NA

## 10 Length of current employment character complete cases complete cases 1000 1.000 5 NA NA

## 11 Instalment per cent character complete cases complete cases 1000 1.000 4 NA NA

## 12 Sex & Marital Status character complete cases complete cases 1000 1.000 4 NA NA

## 13 Guarantors character complete cases complete cases 1000 1.000 3 NA NA

## 14 Duration in Current address character complete cases complete cases 1000 1.000 4 NA NA

## 15 Most valuable available asset character complete cases complete cases 1000 1.000 4 NA NA

## 16 Age (years) numeric special cases special cases 21 0.021 1 Inf NA

## 17 Age (years) numeric complete cases complete cases 979 0.979 53 19 20.00

## 18 Concurrent Credits character complete cases complete cases 1000 1.000 3 NA NA

## 19 Type of apartment character complete cases complete cases 1000 1.000 3 NA NA

## 20 No of Credits at this Bank character complete cases complete cases 1000 1.000 4 NA NA

## 21 Occupation character complete cases complete cases 1000 1.000 4 NA NA

## 22 No of dependents character complete cases complete cases 1000 1.000 2 NA NA

## 23 Telephone character complete cases complete cases 1000 1.000 2 NA NA

## 24 Foreign Worker character complete cases complete cases 1000 1.000 2 NA NA

## p5 p25 p50 avg avg.se p75 p95 p99 max neg pos cnt.outliers sc.ind

## 1 0.00 0.00 0 0.30000 0.01449863 1.00 1.0 1.00 1 0 300 0 0

## 2 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 3 6.00 12.00 18 20.90300 0.38133320 24.00 48.0 60.00 72 0 1000 70 0

## 4 NA NA NA NA NA NA NA NA NA 0 960 NA 0

## 5 NA NA NA NA NA NA NA NA NA NA NA NA 0

## 6 NA NA NA NA NA NA NA NA NA 0 755 NA 0

## 7 NA NA NA NaN NA NA NA NA -Inf NA NA 0 0

## 8 708.45 1371.25 2324 3283.24242 90.03256824 3978.25 9219.7 14194.29 18424 0 990 72 0

## 9 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 10 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 11 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 12 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 13 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 14 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 15 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 16 NA NA NA NaN NA NA NA NA -Inf NA NA 0 0

## 17 22.00 27.00 33 35.52605 0.36315861 42.00 60.0 67.22 75 0 979 23 0

## 18 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 19 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 20 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 21 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 22 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 23 NA NA NA NA NA NA NA NA NA 0 1000 NA 0

## 24 NA NA NA NA NA NA NA NA NA 0 1000 NA 0Based on the results we can see that univariate treats

differently so-called special and complete cases. For result details and

additional arguments of univariate function check help page

?univariate.

From the structure and univariate results, we conclude that there are

four numeric variables, while the rest are categorical. One of the

numeric variables Creditability presents binary indicator

(0/1) of default status which will serve as our dependent variable for

PD model development. The rest of the variables present potential risk

factors for the PD model. Additionally, we see that some risk factors

(Purpose, Credit Amount,

Age (years)) have certain share of special cases and that

for numeric risk factors potential outliers are identified. Sometimes,

analysts want to impute certain values instead of special cases (usually

missing values) as well as for potential outliers. Without going too

much into deeper analysis for this case study we can perform imputations

using two functions from PDtoolkitpackage:

imp.sc for special cases and imp.outliers for

outliers.

#imputation for special cases for risk factors "Credit Amount", "Purpose"

imp.sc.res <- imp.sc(db = loans[, c("Credit Amount", "Purpose")],

method.num = "automatic",

p.val = 0.05)

names(imp.sc.res)## [1] "db" "report"#new risk factors with imputed values

head(imp.sc.res[[1]])## Credit Amount Purpose

## 1 2324 2

## 2 2324 0

## 3 2324 9

## 4 2324 0

## 5 2324 0

## 6 2324 0#imputation report

imp.sc.res[[2]]## rf info imputation.method imputed.value imputation.num imputed.mode

## 1 Credit Amount Imputation completed. automatic - median 2324 10 <NA>

## 2 Purpose Imputation completed. mode NA 21 3#replace Credit Amount and Purpose with new values

loans[, c("Credit Amount", "Purpose")] <- imp.sc.res[[1]]

colSums(is.na(loans))## Creditability Account Balance Duration of Credit (month)

## 0 0 0

## Payment Status of Previous Credit Purpose Credit Amount

## 0 0 0

## Value Savings/Stocks Length of current employment Instalment per cent

## 0 0 0

## Sex & Marital Status Guarantors Duration in Current address

## 0 0 0

## Most valuable available asset Age (years) Concurrent Credits

## 0 21 0

## Type of apartment No of Credits at this Bank Occupation

## 0 0 0

## No of dependents Telephone Foreign Worker

## 0 0 0#imputation for outliers for risk factor Credit Amount

imp.out.res <- imp.outliers(db = loans[, "Credit Amount", drop = FALSE],

method = "iqr",

range = 1.5)

#new risk factors with imputed values

head(imp.out.res[[1]])## Credit Amount

## 1 2324

## 2 2324

## 3 2324

## 4 2324

## 5 2324

## 6 2324#imputation report

imp.out.res[[2]]## rf info imputation.method imputation.val.upper imputation.val.lower

## 1 Credit Amount Imputation completed. iqr 7865 250

## imputation.num.upper imputation.num.lower

## 1 73 0#replace Credit Amount with new values

loans[, "Credit Amount"] <- imp.out.res[[1]]Usually, when building PD models numeric risk factors are

discretized, so we will proceed next with that step. For the purpose of

binning the numeric risk factors, we will use one of the functions

(ndr.bin) from the monobin package. Details

about this package can be found here.

#identify numeric risk factors

num.rf <- sapply(loans, is.numeric)

num.rf <- names(num.rf)[!names(num.rf)%in%"Creditability" & num.rf]

#discretized numeric risk factors using ndr.bin from monobin package

loans[, num.rf] <- sapply(num.rf, function(x)

monobin::ndr.bin(x = loans[, x], y = loans[, "Creditability"])[[2]])

#check loans structure again and confirm binning was sucessful

str(loans)## 'data.frame': 1000 obs. of 21 variables:

## $ Creditability : num 0 0 0 0 0 0 0 0 0 0 ...

## $ Account Balance : chr "1" "1" "2" "1" ...

## $ Duration of Credit (month) : chr "03 [16,45)" "02 [8,16)" "02 [8,16)" "02 [8,16)" ...

## $ Payment Status of Previous Credit: chr "4" "4" "2" "4" ...

## $ Purpose : chr "2" "0" "9" "0" ...

## $ Credit Amount : chr "01 (-Inf,3914)" "01 (-Inf,3914)" "01 (-Inf,3914)" "01 (-Inf,3914)" ...

## $ Value Savings/Stocks : chr "1" "1" "2" "1" ...

## $ Length of current employment : chr "2" "3" "4" "3" ...

## $ Instalment per cent : chr "4" "2" "2" "3" ...

## $ Sex & Marital Status : chr "2" "3" "2" "3" ...

## $ Guarantors : chr "1" "1" "1" "1" ...

## $ Duration in Current address : chr "4" "2" "4" "2" ...

## $ Most valuable available asset : chr "2" "1" "1" "1" ...

## $ Age (years) : chr "01 (-Inf,26)" "03 [35,Inf)" "01 (-Inf,26)" "03 [35,Inf)" ...

## $ Concurrent Credits : chr "3" "3" "3" "3" ...

## $ Type of apartment : chr "1" "1" "1" "1" ...

## $ No of Credits at this Bank : chr "1" "2" "1" "2" ...

## $ Occupation : chr "3" "3" "2" "2" ...

## $ No of dependents : chr "1" "2" "1" "2" ...

## $ Telephone : chr "1" "1" "1" "1" ...

## $ Foreign Worker : chr "1" "1" "1" "2" ...As we can see after the binning, all risk factors are categorical.

Now the modeling data set is ready for bivariate analysis. For that

purpose we will use the function bivariate from the

PDtoolkitpackage.

bivariate(db = loans, target = "Creditability")## $results

## rf bin no ng nb pct.o pct.g pct.b dr so sg

## 1 Account Balance 1 274 139 135 0.274 0.198571429 0.450000000 0.4927007 1000 700

## 2 Account Balance 2 269 164 105 0.269 0.234285714 0.350000000 0.3903346 1000 700

## 3 Account Balance 3 63 49 14 0.063 0.070000000 0.046666667 0.2222222 1000 700

## 4 Account Balance 4 394 348 46 0.394 0.497142857 0.153333333 0.1167513 1000 700

## 5 Duration of Credit (month) 01 (-Inf,8) 87 78 9 0.087 0.111428571 0.030000000 0.1034483 1000 700

## 6 Duration of Credit (month) 02 [8,16) 344 264 80 0.344 0.377142857 0.266666667 0.2325581 1000 700

## 7 Duration of Credit (month) 03 [16,45) 499 328 171 0.499 0.468571429 0.570000000 0.3426854 1000 700

## 8 Duration of Credit (month) 04 [45,Inf) 70 30 40 0.070 0.042857143 0.133333333 0.5714286 1000 700

## 9 Payment Status of Previous Credit 0 40 15 25 0.040 0.021428571 0.083333333 0.6250000 1000 700

## 10 Payment Status of Previous Credit 1 49 21 28 0.049 0.030000000 0.093333333 0.5714286 1000 700

## 11 Payment Status of Previous Credit 2 530 361 169 0.530 0.515714286 0.563333333 0.3188679 1000 700

## 12 Payment Status of Previous Credit 3 88 60 28 0.088 0.085714286 0.093333333 0.3181818 1000 700

## 13 Payment Status of Previous Credit 4 293 243 50 0.293 0.347142857 0.166666667 0.1706485 1000 700

## 14 Purpose 0 224 145 79 0.224 0.207142857 0.263333333 0.3526786 1000 700

## 15 Purpose 1 102 86 16 0.102 0.122857143 0.053333333 0.1568627 1000 700

## 16 Purpose 10 12 7 5 0.012 0.010000000 0.016666667 0.4166667 1000 700

## 17 Purpose 2 177 123 54 0.177 0.175714286 0.180000000 0.3050847 1000 700

## 18 Purpose 3 300 218 82 0.300 0.311428571 0.273333333 0.2733333 1000 700

## 19 Purpose 4 12 8 4 0.012 0.011428571 0.013333333 0.3333333 1000 700

## 20 Purpose 5 21 14 7 0.021 0.020000000 0.023333333 0.3333333 1000 700

## 21 Purpose 6 49 28 21 0.049 0.040000000 0.070000000 0.4285714 1000 700

## 22 Purpose 8 9 8 1 0.009 0.011428571 0.003333333 0.1111111 1000 700

## 23 Purpose 9 94 63 31 0.094 0.090000000 0.103333333 0.3297872 1000 700

## 24 Credit Amount 01 (-Inf,3914) 739 550 189 0.739 0.785714286 0.630000000 0.2557510 1000 700

## 25 Credit Amount 02 [3914,Inf) 261 150 111 0.261 0.214285714 0.370000000 0.4252874 1000 700

## 26 Value Savings/Stocks 1 603 386 217 0.603 0.551428571 0.723333333 0.3598673 1000 700

## 27 Value Savings/Stocks 2 103 69 34 0.103 0.098571429 0.113333333 0.3300971 1000 700

## 28 Value Savings/Stocks 3 63 52 11 0.063 0.074285714 0.036666667 0.1746032 1000 700

## 29 Value Savings/Stocks 4 48 42 6 0.048 0.060000000 0.020000000 0.1250000 1000 700

## 30 Value Savings/Stocks 5 183 151 32 0.183 0.215714286 0.106666667 0.1748634 1000 700

## 31 Length of current employment 1 62 39 23 0.062 0.055714286 0.076666667 0.3709677 1000 700

## 32 Length of current employment 2 172 102 70 0.172 0.145714286 0.233333333 0.4069767 1000 700

## 33 Length of current employment 3 339 235 104 0.339 0.335714286 0.346666667 0.3067847 1000 700

## 34 Length of current employment 4 174 135 39 0.174 0.192857143 0.130000000 0.2241379 1000 700

## 35 Length of current employment 5 253 189 64 0.253 0.270000000 0.213333333 0.2529644 1000 700

## 36 Instalment per cent 1 136 102 34 0.136 0.145714286 0.113333333 0.2500000 1000 700

## 37 Instalment per cent 2 231 169 62 0.231 0.241428571 0.206666667 0.2683983 1000 700

## 38 Instalment per cent 3 157 112 45 0.157 0.160000000 0.150000000 0.2866242 1000 700

## 39 Instalment per cent 4 476 317 159 0.476 0.452857143 0.530000000 0.3340336 1000 700

## 40 Sex & Marital Status 1 50 30 20 0.050 0.042857143 0.066666667 0.4000000 1000 700

## 41 Sex & Marital Status 2 310 201 109 0.310 0.287142857 0.363333333 0.3516129 1000 700

## 42 Sex & Marital Status 3 548 402 146 0.548 0.574285714 0.486666667 0.2664234 1000 700

## 43 Sex & Marital Status 4 92 67 25 0.092 0.095714286 0.083333333 0.2717391 1000 700

## 44 Guarantors 1 907 635 272 0.907 0.907142857 0.906666667 0.2998897 1000 700

## 45 Guarantors 2 41 23 18 0.041 0.032857143 0.060000000 0.4390244 1000 700

## 46 Guarantors 3 52 42 10 0.052 0.060000000 0.033333333 0.1923077 1000 700

## 47 Duration in Current address 1 130 94 36 0.130 0.134285714 0.120000000 0.2769231 1000 700

## 48 Duration in Current address 2 308 211 97 0.308 0.301428571 0.323333333 0.3149351 1000 700

## 49 Duration in Current address 3 149 106 43 0.149 0.151428571 0.143333333 0.2885906 1000 700

## 50 Duration in Current address 4 413 289 124 0.413 0.412857143 0.413333333 0.3002421 1000 700

## 51 Most valuable available asset 1 282 222 60 0.282 0.317142857 0.200000000 0.2127660 1000 700

## 52 Most valuable available asset 2 232 161 71 0.232 0.230000000 0.236666667 0.3060345 1000 700

## 53 Most valuable available asset 3 332 230 102 0.332 0.328571429 0.340000000 0.3072289 1000 700

## 54 Most valuable available asset 4 154 87 67 0.154 0.124285714 0.223333333 0.4350649 1000 700

## 55 Age (years) 01 (-Inf,26) 187 108 79 0.187 0.154285714 0.263333333 0.4224599 1000 700

## 56 Age (years) 02 [26,35) 349 238 111 0.349 0.340000000 0.370000000 0.3180516 1000 700

## 57 Age (years) 03 [35,Inf) 443 335 108 0.443 0.478571429 0.360000000 0.2437923 1000 700

## 58 Age (years) SC 21 19 2 0.021 0.027142857 0.006666667 0.0952381 1000 700

## 59 Concurrent Credits 1 139 82 57 0.139 0.117142857 0.190000000 0.4100719 1000 700

## 60 Concurrent Credits 2 47 28 19 0.047 0.040000000 0.063333333 0.4042553 1000 700

## 61 Concurrent Credits 3 814 590 224 0.814 0.842857143 0.746666667 0.2751843 1000 700

## 62 Type of apartment 1 179 109 70 0.179 0.155714286 0.233333333 0.3910615 1000 700

## 63 Type of apartment 2 714 528 186 0.714 0.754285714 0.620000000 0.2605042 1000 700

## 64 Type of apartment 3 107 63 44 0.107 0.090000000 0.146666667 0.4112150 1000 700

## 65 No of Credits at this Bank 1 633 433 200 0.633 0.618571429 0.666666667 0.3159558 1000 700

## 66 No of Credits at this Bank 2 333 241 92 0.333 0.344285714 0.306666667 0.2762763 1000 700

## 67 No of Credits at this Bank 3 28 22 6 0.028 0.031428571 0.020000000 0.2142857 1000 700

## 68 No of Credits at this Bank 4 6 4 2 0.006 0.005714286 0.006666667 0.3333333 1000 700

## 69 Occupation 1 22 15 7 0.022 0.021428571 0.023333333 0.3181818 1000 700

## 70 Occupation 2 200 144 56 0.200 0.205714286 0.186666667 0.2800000 1000 700

## 71 Occupation 3 630 444 186 0.630 0.634285714 0.620000000 0.2952381 1000 700

## 72 Occupation 4 148 97 51 0.148 0.138571429 0.170000000 0.3445946 1000 700

## 73 No of dependents 1 845 591 254 0.845 0.844285714 0.846666667 0.3005917 1000 700

## 74 No of dependents 2 155 109 46 0.155 0.155714286 0.153333333 0.2967742 1000 700

## 75 Telephone 1 596 409 187 0.596 0.584285714 0.623333333 0.3137584 1000 700

## 76 Telephone 2 404 291 113 0.404 0.415714286 0.376666667 0.2797030 1000 700

## 77 Foreign Worker 1 963 667 296 0.963 0.952857143 0.986666667 0.3073728 1000 700

## 78 Foreign Worker 2 37 33 4 0.037 0.047142857 0.013333333 0.1081081 1000 700

## sb dist.g dist.b woe iv.b iv.s auc

## 1 300 0.198571429 0.450000000 -0.8180987057 0.2056933888604 0.66601150335 0.7077690

## 2 300 0.234285714 0.350000000 -0.4013917827 0.0464467634291 0.66601150335 0.7077690

## 3 300 0.070000000 0.046666667 0.4054651081 0.0094608525225 0.66601150335 0.7077690

## 4 300 0.497142857 0.153333333 1.1762632229 0.4044104985393 0.66601150335 0.7077690

## 5 300 0.111428571 0.030000000 1.3121863890 0.1068494631015 0.26770659621 0.6241762

## 6 300 0.377142857 0.266666667 0.3466246081 0.0382937662266 0.26770659621 0.6241762

## 7 300 0.468571429 0.570000000 -0.1959478085 0.0198747062913 0.26770659621 0.6241762

## 8 300 0.042857143 0.133333333 -1.1349799328 0.1026886605902 0.26770659621 0.6241762

## 9 300 0.021428571 0.083333333 -1.3581234842 0.0840743109238 0.29323354739 0.6268048

## 10 300 0.030000000 0.093333333 -1.1349799328 0.0718820624131 0.29323354739 0.6268048

## 11 300 0.515714286 0.563333333 -0.0883186170 0.0042056484275 0.29323354739 0.6268048

## 12 300 0.085714286 0.093333333 -0.0851578083 0.0006488213969 0.29323354739 0.6268048

## 13 300 0.347142857 0.166666667 0.7337405775 0.1324227042295 0.29323354739 0.6268048

## 14 300 0.207142857 0.263333333 -0.2400119704 0.0134863869101 0.10939307333 0.5821500

## 15 300 0.122857143 0.053333333 0.8344607136 0.0580148877093 0.10939307333 0.5821500

## 16 300 0.010000000 0.016666667 -0.5108256238 0.0034055041584 0.10939307333 0.5821500

## 17 300 0.175714286 0.180000000 -0.0240975516 0.0001032752211 0.10939307333 0.5821500

## 18 300 0.311428571 0.273333333 0.1304779551 0.0049705887671 0.10939307333 0.5821500

## 19 300 0.011428571 0.013333333 -0.1541506798 0.0002936203425 0.10939307333 0.5821500

## 20 300 0.020000000 0.023333333 -0.1541506798 0.0005138355994 0.10939307333 0.5821500

## 21 300 0.040000000 0.070000000 -0.5596157879 0.0167884736381 0.10939307333 0.5821500

## 22 300 0.011428571 0.003333333 1.2321436813 0.0099744964676 0.10939307333 0.5821500

## 23 300 0.090000000 0.103333333 -0.1381503385 0.0018420045131 0.10939307333 0.5821500

## 24 300 0.785714286 0.630000000 0.2208734028 0.0343931441471 0.11944316082 0.5778571

## 25 300 0.214285714 0.370000000 -0.5461927676 0.0850500166697 0.11944316082 0.5778571

## 26 300 0.551428571 0.723333333 -0.2713578445 0.0466477056434 0.19600955690 0.5991429

## 27 300 0.098571429 0.113333333 -0.1395518804 0.0020600515679 0.19600955690 0.5991429

## 28 300 0.074285714 0.036666667 0.7060505854 0.0265609505935 0.19600955690 0.5991429

## 29 300 0.060000000 0.020000000 1.0986122887 0.0439444915467 0.19600955690 0.5991429

## 30 300 0.215714286 0.106666667 0.7042460736 0.0767963575528 0.19600955690 0.5991429

## 31 300 0.055714286 0.076666667 -0.3192304302 0.0066886375849 0.08643363103 0.5808190

## 32 300 0.145714286 0.233333333 -0.4708202892 0.0412528253352 0.08643363103 0.5808190

## 33 300 0.335714286 0.346666667 -0.0321032454 0.0003516069733 0.08643363103 0.5808190

## 34 300 0.192857143 0.130000000 0.3944152719 0.0247918170922 0.08643363103 0.5808190

## 35 300 0.270000000 0.213333333 0.2355660713 0.0133487440411 0.08643363103 0.5808190

## 36 300 0.145714286 0.113333333 0.2513144283 0.0081378005348 0.02632209005 0.5433833

## 37 300 0.241428571 0.206666667 0.1554664695 0.0054043106061 0.02632209005 0.5433833

## 38 300 0.160000000 0.150000000 0.0645385211 0.0006453852114 0.02632209005 0.5433833

## 39 300 0.452857143 0.530000000 -0.1573002887 0.0121345937020 0.02632209005 0.5433833

## 40 300 0.042857143 0.066666667 -0.4418327523 0.0105198274352 0.04467067763 0.5524238

## 41 300 0.287142857 0.363333333 -0.2353408346 0.0179307302520 0.04467067763 0.5524238

## 42 300 0.574285714 0.486666667 0.1655476065 0.0145051236192 0.04467067763 0.5524238

## 43 300 0.095714286 0.083333333 0.1385189341 0.0017149963274 0.04467067763 0.5524238

## 44 300 0.907142857 0.906666667 0.0005250722 0.0000002500344 0.03201932202 0.5256524

## 45 300 0.032857143 0.060000000 -0.6021754024 0.0163447609210 0.03201932202 0.5256524

## 46 300 0.060000000 0.033333333 0.5877866649 0.0156743110641 0.03201932202 0.5256524

## 47 300 0.134285714 0.120000000 0.1124779834 0.0016068283347 0.00358877319 0.5161786

## 48 300 0.301428571 0.323333333 -0.0701507054 0.0015366344996 0.00358877319 0.5161786

## 49 300 0.151428571 0.143333333 0.0549411180 0.0004447614317 0.00358877319 0.5161786

## 50 300 0.412857143 0.413333333 -0.0011527379 0.0000005489228 0.00358877319 0.5161786

## 51 300 0.317142857 0.200000000 0.4610349593 0.0540069523708 0.11263826241 0.5853286

## 52 300 0.230000000 0.236666667 -0.0285733724 0.0001904891496 0.11263826241 0.5853286

## 53 300 0.328571429 0.340000000 -0.0341913647 0.0003907584543 0.11263826241 0.5853286

## 54 300 0.124285714 0.223333333 -0.5860823611 0.0580500624351 0.11263826241 0.5853286

## 55 300 0.154285714 0.263333333 -0.5346144857 0.0582984367772 0.12334106269 0.5890381

## 56 300 0.340000000 0.370000000 -0.0845573880 0.0025367216408 0.12334106269 0.5890381

## 57 300 0.478571429 0.360000000 0.2847014443 0.0337574569686 0.12334106269 0.5890381

## 58 300 0.027142857 0.006666667 1.4039939382 0.0287484473064 0.12334106269 0.5890381

## 59 300 0.117142857 0.190000000 -0.4836298810 0.0352358913269 0.05761454196 0.5481857

## 60 300 0.040000000 0.063333333 -0.4595323294 0.0107224210188 0.05761454196 0.5481857

## 61 300 0.842857143 0.746666667 0.1211786247 0.0116562296099 0.05761454196 0.5481857

## 62 300 0.155714286 0.233333333 -0.4044452202 0.0313926528066 0.08539292555 0.5680619

## 63 300 0.754285714 0.620000000 0.1960517496 0.0263269492328 0.08539292555 0.5680619

## 64 300 0.090000000 0.146666667 -0.4883527679 0.0276733235151 0.08539292555 0.5680619

## 65 300 0.618571429 0.666666667 -0.0748774989 0.0036012511391 0.01326652424 0.5260571

## 66 300 0.344285714 0.306666667 0.1157104961 0.0043529186611 0.01326652424 0.5260571

## 67 300 0.031428571 0.020000000 0.4519851237 0.0051655442713 0.01326652424 0.5260571

## 68 300 0.005714286 0.006666667 -0.1541506798 0.0001468101713 0.01326652424 0.5260571

## 69 300 0.021428571 0.023333333 -0.0851578083 0.0001622053492 0.00876276571 0.5214429

## 70 300 0.205714286 0.186666667 0.0971637485 0.0018507380658 0.00876276571 0.5214429

## 71 300 0.634285714 0.620000000 0.0227800283 0.0003254289762 0.00876276571 0.5214429

## 72 300 0.138571429 0.170000000 -0.2044125146 0.0064243933163 0.00876276571 0.5214429

## 73 300 0.844285714 0.846666667 -0.0028161100 0.0000067050238 0.00004339223 0.5011905

## 74 300 0.155714286 0.153333333 0.0154086254 0.0000366872032 0.00004339223 0.5011905

## 75 300 0.584285714 0.623333333 -0.0646913212 0.0025260420659 0.00637760503 0.5195238

## 76 300 0.415714286 0.376666667 0.0986375881 0.0038515629628 0.00637760503 0.5195238

## 77 300 0.952857143 0.986666667 -0.0348672688 0.0011788457545 0.04387741201 0.5169048

## 78 300 0.047142857 0.013333333 1.2629153400 0.0426985662558 0.04387741201 0.5169048

##

## $info

## data frame with 0 columns and 0 rowsBased on results of the bivariate analysis we can see that risk

factor Purpose has 10 modalities, that

Age (years) has share of special cases 2.1% and that there

are quite some other risk factors with modality share less than 5%. In

order to correct above potential issues, we can further categorize risk

factors Purpose, Foreign Worker

and Age (years) given the following criteria:

For this purpose we will use function cat.bin.

Additional examples of cat.bin function usage can be found

in its help page ?cat.bin. Note: Usually in

the practice greater attention is paid on this step and all risk factors

are examined closer.

rf <- c("Purpose", "Age (years)", "Foreign Worker")

loans[, rf] <- sapply(rf, function(x)

cat.bin(x = loans[, x],

y = loans[, "Creditability"],

sc = c("SC", NA),

sc.merge = "closest",

min.pct.obs = 0.05,

min.avg.rate = 0.01,

max.groups = 5,

force.trend = "dr")[[2]])

#run bivariate analysis again

bivariate(db = loans[, c(rf, "Creditability")], target = "Creditability")## $results

## rf bin no ng nb pct.o pct.g pct.b dr so sg sb dist.g

## 1 Purpose 1 [1,8] 111 94 17 0.111 0.1342857 0.05666667 0.1531532 1000 700 300 0.1342857

## 2 Purpose 2 [3] 300 218 82 0.300 0.3114286 0.27333333 0.2733333 1000 700 300 0.3114286

## 3 Purpose 3 [2] 177 123 54 0.177 0.1757143 0.18000000 0.3050847 1000 700 300 0.1757143

## 4 Purpose 4 [0,4,5,9] 351 230 121 0.351 0.3285714 0.40333333 0.3447293 1000 700 300 0.3285714

## 5 Purpose 5 [10,6] 61 35 26 0.061 0.0500000 0.08666667 0.4262295 1000 700 300 0.0500000

## 6 Age (years) 1 [01 (-Inf,26)] 187 108 79 0.187 0.1542857 0.26333333 0.4224599 1000 700 300 0.1542857

## 7 Age (years) 2 [02 [26,35)] 349 238 111 0.349 0.3400000 0.37000000 0.3180516 1000 700 300 0.3400000

## 8 Age (years) 3 [03 [35,Inf)] 464 354 110 0.464 0.5057143 0.36666667 0.2370690 1000 700 300 0.5057143

## 9 Foreign Worker 1 [2,1] 1000 700 300 1.000 1.0000000 1.00000000 0.3000000 1000 700 300 1.0000000

## dist.b woe iv.b iv.s auc

## 1 0.05666667 0.86278358 0.0669684396 0.1075375 0.5805190

## 2 0.27333333 0.13047796 0.0049705888 0.1075375 0.5805190

## 3 0.18000000 -0.02409755 0.0001032752 0.1075375 0.5805190

## 4 0.40333333 -0.20500910 0.0153268706 0.1075375 0.5805190

## 5 0.08666667 -0.55004634 0.0201683657 0.1075375 0.5805190

## 6 0.26333333 -0.53461449 0.0582984368 0.1055416 0.5857476

## 7 0.37000000 -0.08455739 0.0025367216 0.1055416 0.5857476

## 8 0.36666667 0.32151869 0.0447064079 0.1055416 0.5857476

## 9 1.00000000 0.00000000 0.0000000000 0.0000000 NA

##

## $info

## data frame with 0 columns and 0 rowsAfter additional binning based on above criteria and running again

the bivariate analysis, we see that risk factor

Foreign Worker has only one value and it can be discarded

from the further analysis.

loans <- loans[, !names(loans)%in%"Foreign Worker"]In case when too many risk factors are available, analysts have an

option to perform cluster analysis and shorten the list of potential

candidates for final PD model. For this purpose, PDtoolkit

package contains function rf.clustering. Since the most

metrics needed for distance matrix calculation require numeric values,

we will first replace risk factors’ modalities with Weights of Evidence

(WoE) and then perform clustering.

#replace modalities with WoE

woe.res <- replace.woe(db = loans, target = "Creditability")

head(woe.res[[1]])## Creditability Account Balance Duration of Credit (month) Payment Status of Previous Credit Purpose

## 1 0 -0.8180987 -0.1959478 0.73374058 -0.02409755

## 2 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## 3 0 -0.4013918 0.3466246 -0.08831862 -0.20500910

## 4 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## 5 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## 6 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## Credit Amount Value Savings/Stocks Length of current employment Instalment per cent Sex & Marital Status

## 1 0.2208734 -0.2713578 -0.47082029 -0.15730029 -0.2353408

## 2 0.2208734 -0.2713578 -0.03210325 0.15546647 0.1655476

## 3 0.2208734 -0.1395519 0.39441527 0.15546647 -0.2353408

## 4 0.2208734 -0.2713578 -0.03210325 0.06453852 0.1655476

## 5 0.2208734 -0.2713578 -0.03210325 -0.15730029 0.1655476

## 6 0.2208734 -0.2713578 -0.47082029 0.25131443 0.1655476

## Guarantors Duration in Current address Most valuable available asset Age (years) Concurrent Credits

## 1 0.0005250722 -0.001152738 -0.02857337 -0.5346145 0.1211786

## 2 0.0005250722 -0.070150705 0.46103496 0.3215187 0.1211786

## 3 0.0005250722 -0.001152738 0.46103496 -0.5346145 0.1211786

## 4 0.0005250722 -0.070150705 0.46103496 0.3215187 0.1211786

## 5 0.0005250722 -0.001152738 -0.02857337 0.3215187 -0.4836299

## 6 0.0005250722 0.054941118 0.46103496 0.3215187 0.1211786

## Type of apartment No of Credits at this Bank Occupation No of dependents Telephone

## 1 -0.4044452 -0.0748775 0.02278003 -0.00281611 -0.06469132

## 2 -0.4044452 0.1157105 0.02278003 0.01540863 -0.06469132

## 3 -0.4044452 -0.0748775 0.09716375 -0.00281611 -0.06469132

## 4 -0.4044452 0.1157105 0.09716375 0.01540863 -0.06469132

## 5 0.1960517 0.1157105 0.09716375 -0.00281611 -0.06469132

## 6 -0.4044452 0.1157105 0.09716375 0.01540863 -0.06469132loans.woe <- woe.res[[1]]

#perform cluster analysis using "common pearson" metric

#number of clusters is set to NA in order to enable automatic determination of optimal number of clusters using elbow method

rf.clustering(db = loans.woe, metric = "common pearson", k = NA)## rf clusters dist.to.centroid

## 1 Creditability 1 0.0000000

## 2 Account Balance 2 0.0000000

## 4 Duration of Credit (month) 3 0.5788368

## 6 Occupation 3 0.6001961

## 3 Credit Amount 3 0.6892248

## 7 Type of apartment 3 0.7067914

## 5 Most valuable available asset 3 0.8086682

## 8 Payment Status of Previous Credit 4 0.0000000

## 9 Purpose 5 0.0000000

## 10 Value Savings/Stocks 6 0.0000000

## 11 Length of current employment 7 0.0000000

## 12 Instalment per cent 8 0.0000000

## 13 Sex & Marital Status 9 0.0000000

## 14 Guarantors 10 0.0000000

## 15 Duration in Current address 11 0.0000000

## 16 Age (years) 12 0.0000000

## 17 Concurrent Credits 13 0.0000000

## 18 No of Credits at this Bank 14 0.0000000

## 19 No of dependents 15 0.0000000

## 20 Telephone 16 0.0000000Beside metrics that require numeric inputs, there is x2y

metric that works with both numeric and categorical data. This metric is

especially handy if analyst wants to perform clustering before any

binning procedures and to decrease the number of risk factors. More

examples of the clustering can be found in help page

?rf.clustering, while the details about x2y

metric are presented in this link.

Due to the fact that for this example we don’t have too many risk factors, we will not use the results of cluster analysis to shorten the list of potential risk factors for the final PD model.

The next step is then to perform multivariate analysis and to select

the final PD model. In order to complete this task we will use function

stepMIV. This function uses the concept of Marginal

Information Value (MIV) in order to select risk factors in the model.

Details can be found on the help page of the function

?stepMIV.

multiv.res <- stepMIV(start.model = Creditability ~ 1,

miv.threshold = 0.02,

m.ch.p.val = 0.05,

coding = "WoE",

db = loans)## [1] "Running iteration: 1"

## [1] "Running iteration: 2"

## [1] "Running iteration: 3"

## [1] "Running iteration: 4"

## [1] "Running iteration: 5"

## [1] "Running iteration: 6"

## [1] "Running iteration: 7"#print the output elements

names(multiv.res)## [1] "model" "steps" "miv.iter" "warnings" "dev.db"#print the final model and estimated coefficients

multiv.res$model##

## Call: glm(formula = as.formula(mod.frm), family = "binomial", data = db)

##

## Coefficients:

## (Intercept) `Account Balance` `Duration of Credit (month)`

## -0.8386 -0.8516 -0.9586

## `Payment Status of Previous Credit` `Value Savings/Stocks` Purpose

## -0.7857 -0.7754 -0.9566

## Guarantors

## -1.1917

##

## Degrees of Freedom: 999 Total (i.e. Null); 993 Residual

## Null Deviance: 1222

## Residual Deviance: 973.6 AIC: 987.6summary(multiv.res$model)$coefficients## Estimate Std. Error z value Pr(>|z|)

## (Intercept) -0.8385682 0.08070531 -10.390496 2.739256e-25

## `Account Balance` -0.8515981 0.10201758 -8.347562 6.968627e-17

## `Duration of Credit (month)` -0.9586008 0.16294350 -5.883026 4.028332e-09

## `Payment Status of Previous Credit` -0.7856716 0.14969919 -5.248336 1.534793e-07

## `Value Savings/Stocks` -0.7754343 0.19240625 -4.030193 5.573104e-05

## Purpose -0.9565752 0.25273860 -3.784840 1.538075e-04

## Guarantors -1.1916767 0.42403712 -2.810312 4.949344e-03#store the final model

pd.model <- multiv.res$model

#store the data set used for the model estimation

pd.db <- multiv.res$dev.db

#note that risk factors from the model are coded using WoE due to the fact that WoE coding method is used in stepMIV estimation

head(pd.db)## Creditability Account Balance Duration of Credit (month) Payment Status of Previous Credit Purpose

## 1 0 -0.8180987 -0.1959478 0.73374058 -0.02409755

## 2 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## 3 0 -0.4013918 0.3466246 -0.08831862 -0.20500910

## 4 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## 5 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## 6 0 -0.8180987 0.3466246 0.73374058 -0.20500910

## Credit Amount Value Savings/Stocks Length of current employment Instalment per cent Sex & Marital Status

## 1 01 (-Inf,3914) -0.2713578 2 4 2

## 2 01 (-Inf,3914) -0.2713578 3 2 3

## 3 01 (-Inf,3914) -0.1395519 4 2 2

## 4 01 (-Inf,3914) -0.2713578 3 3 3

## 5 01 (-Inf,3914) -0.2713578 3 4 3

## 6 01 (-Inf,3914) -0.2713578 2 1 3

## Guarantors Duration in Current address Most valuable available asset Age (years) Concurrent Credits

## 1 0.0005250722 4 2 1 [01 (-Inf,26)] 3

## 2 0.0005250722 2 1 3 [03 [35,Inf)] 3

## 3 0.0005250722 4 1 1 [01 (-Inf,26)] 3

## 4 0.0005250722 2 1 3 [03 [35,Inf)] 3

## 5 0.0005250722 4 2 3 [03 [35,Inf)] 1

## 6 0.0005250722 3 1 3 [03 [35,Inf)] 3

## Type of apartment No of Credits at this Bank Occupation No of dependents Telephone

## 1 1 1 3 1 1

## 2 1 2 3 2 1

## 3 1 1 2 1 1

## 4 1 2 2 2 1

## 5 2 2 2 1 1

## 6 1 2 2 2 1#calculate area under curve (AUC) for the final model

auc.model(predictions = predict(pd.model, type = "response", newdata = pd.db),

observed = pd.db$Creditability)## [1] 0.7983738In practice multivariate analysis is highly iterative process, so

analysts usually end up with a few candidate models. After that based on

different statistical and business validations of these models, one is

selected as the final. For the further process we will assume that the

model from the previous step is the final and proceed with its

validation. For that purpose, we will apply k-fold cross-validation and

validation based on bootstrapping. Both methods are implemented in

PDtoolkit package, concretely in functions

kfold.vld and boots.vld.

kfold.vld.res <- kfold.vld(model = pd.model, k = 10, seed = 1984)

kfold.vld.res## $iter

## k no amse rmse auc

## 1 1 100 0.1630258 0.4037645 0.7712482

## 2 2 100 0.1374731 0.3707736 0.8635211

## 3 3 100 0.1908883 0.4369077 0.7076403

## 4 4 100 0.1179182 0.3433922 0.8726708

## 5 5 100 0.1880557 0.4336539 0.7256897

## 6 6 100 0.1637761 0.4046927 0.8037087

## 7 7 100 0.1400881 0.3742835 0.8508985

## 8 8 100 0.1827844 0.4275329 0.8596527

## 9 9 100 0.1910433 0.4370850 0.7354138

## 10 10 100 0.1617250 0.4021504 0.7536383

##

## $summary

## amse rmse auc

## 1 0.1636778 0.4034236 0.7944082boots.vld.res <- boots.vld (model = pd.model, B = 10, seed = 1122)

head(boots.vld.res[[1]])## B amse rmse auc

## 1 1 0.1555666 0.3944193 0.8057968

## 2 2 0.1620125 0.4025078 0.7944065

## 3 3 0.1555915 0.3944509 0.8093665

## 4 4 0.1705968 0.4130337 0.7788997

## 5 5 0.1491317 0.3861758 0.8268758

## 6 6 0.1559972 0.3949648 0.8033898boots.vld.res[[2]]## amse rmse auc

## 1 0.1603226 0.4002763 0.7975205After validating performance metrics from the previous step, we would

like to test if there are some segments within modeling data set where

our final model significantly overestimates or underestimates observed

defaults. This can be achieved using function segment.vld,

also implemented in PDtoolkit package.

segment.vld(model = pd.model,

db = pd.db,

alpha = 0.05)## $segment.model

## n= 1000

##

## node), split, n, deviance, yval

## * denotes terminal node

##

## 1) root 1000 160.705 -0.000000000000002700284 *

##

## $segment.testing

## info

## 1 No significant split of residuals.

##

## $segment.rules

## NULLFor more examples check help page ?segment.vld. After

decision on the final model, analysts usually transform model

probabilities into scaled scores and form the rating scale. Next example

presents the way to accomplish these two tasks using

PDtoolkit and monobin package.

#extract model predictions

pd.db$probs <- unname(predict(pd.model, type = "response", newdata = pd.db))

#scale probabilities (note: higher score lower probability)

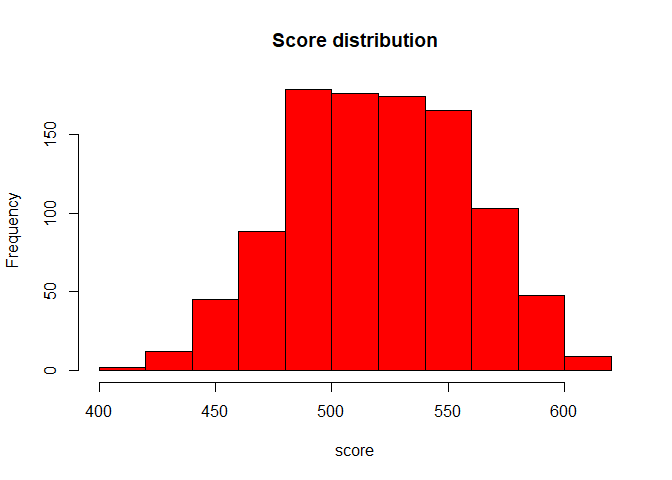

pd.db$score <- round(scaled.score(probs = pd.db$probs, score = 600, odd = 50/1, pdo = 20), 0)

hist(pd.db$score, col = "red", main = "Score distribution", xlab = "score")

#create ratings based on binning algorithm

pd.db$rating <- monobin::sts.bin(x = pd.db$score, y = pd.db$Creditability, y.type = "bina")[[2]]

#summarise rating scale

rs <- pd.db %>%

group_by(rating) %>%

summarise(no = n(),

nb = sum(Creditability),

ng = sum(1 - Creditability)) %>%

mutate(dr = nb / no)

rs## # A tibble: 6 x 5

## rating no nb ng dr

## <chr> <int> <dbl> <dbl> <dbl>

## 1 01 (-Inf,473) 99 75 24 0.758

## 2 02 [473,482) 72 46 26 0.639

## 3 03 [482,506) 196 83 113 0.423

## 4 04 [506,515) 100 30 70 0.3

## 5 05 [515,547) 267 52 215 0.195

## 6 06 [547,Inf) 266 14 252 0.0526Often default rate from the modeling data set differs from the

so-called portfolio central tendency (in practice known as long-run

average). Without going deeper into reasons and direction of this

difference we will assume that central tendency for this case study is

27% and re-calibrate our rating scale. In order to do so, we will use

rs.calibration function from PDtoolkit

package. For details on calibration options check its help page

?rs.calibration.

rs$pd <- rs.calibration(rs = rs,

dr = "dr",

w = "no",

ct = 0.27,

min.pd = 0.05,

method = "log.odds.ab")

rs## # A tibble: 6 x 6

## rating no nb ng dr pd

## <chr> <int> <dbl> <dbl> <dbl> <dbl>

## 1 01 (-Inf,473) 99 75 24 0.758 0.740

## 2 02 [473,482) 72 46 26 0.639 0.607

## 3 03 [482,506) 196 83 113 0.423 0.375

## 4 04 [506,515) 100 30 70 0.3 0.252

## 5 05 [515,547) 267 52 215 0.195 0.154

## 6 06 [547,Inf) 266 14 252 0.0526 0.05#check if calibration is performed as expected

sum(rs$pd * rs$no) / sum(rs$no)## [1] 0.27#plot main rating scale characteristics

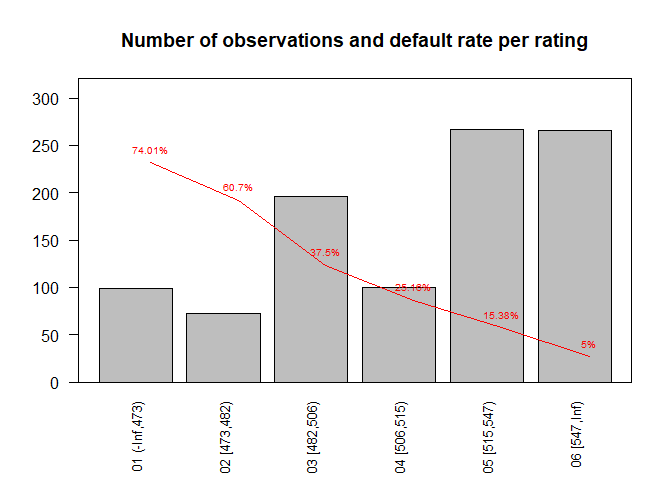

bp <- barplot(rs$no, names.arg = rs$rating, cex.names = 0.8, las = 2, ylim = c(0, max(rs$no) * 1.2),

main = "Number of observations and default rate per rating")

xlim <- c(floor(min(bp)), ceiling(max(bp)))

par(new = TRUE)

plot(bp, rs$pd, type = "l", col = "red", xaxt = "n", yaxt = "n",

xlab = "", ylab = "", xlim = xlim, ylim = c(0, 1))

text(x = bp, y = rs$pd, label = paste0(round(100 * rs$pd, 2), "%"), col = "red",

cex = 0.6, pos = 3)

#bring PDs to the modeling data set and calculate AUC

pd.db <- merge(pd.db, rs[, c("rating", "pd")], by = "rating", all.x = TRUE)

auc.model(predictions = pd.db$pd, observed = pd.db$Creditability)## [1] 0.79465After finalization of PD model development, analysts have to perform

regular validation of the model performance. Model validation is

performed at least on yearly basis on so-called application portfolio.

PDtoolkit has set of functions that are useful for model

validation and next steps present its usage. Before implementation of

any of the validation tests, let’s simulate application portfolio.

set.seed(112233)

app.port <- pd.db[sample(1:nrow(pd.db), 500, replace = FALSE), ]Now, let’s perform heterogeneity test of the rating scale in order to check if the model still discriminates well between rating grades. This validation procedure applies test of two proportions on adjacent rating grades and check if there is statistical significant difference between observed default rates. It is always one-tail test, but direction depends on direction of default rate per rating (increasing or decreasing).

heterogeneity(app.port = app.port,

def.ind = "Creditability",

rating = "rating",

alpha = 0.05)## rating no nb dr p.val alpha res

## 1 01 (-Inf,473) 47 36 0.76595745 NA 0.05 <NA>

## 2 02 [473,482) 35 21 0.60000000 0.05319294 0.05 H0: DR(02 [473,482)) >= DR(01 (-Inf,473))

## 3 03 [482,506) 93 37 0.39784946 0.02028868 0.05 H1: DR(03 [482,506)) < DR(02 [473,482))

## 4 04 [506,515) 53 15 0.28301887 0.08176299 0.05 H0: DR(04 [506,515)) >= DR(03 [482,506))

## 5 05 [515,547) 131 22 0.16793893 0.03889198 0.05 H1: DR(05 [515,547)) < DR(04 [506,515))

## 6 06 [547,Inf) 141 11 0.07801418 0.01161535 0.05 H1: DR(06 [547,Inf)) < DR(05 [515,547))Based on the results we can see that there are two pairs of rating grades where we cannot conclude that observed default rate in the second rating grade is less than observed default rate in the previous rating grade. These two pairs are:

Usually in practice the further investigation is performed in order

to better understand source of poor discrimination between these two

rating pairs. Due to the fact that application portfolio in this

example does not have enough observations to perform homogeneity test,

the help page of the ?homogeneity function contains

examples, details and design behind the implemented test. Closely

related validation procedure to heterogeneity and homogeneity is

validation of discriminatory power of the PD model. Namely, analysts

usually have to validate and make sure that discriminatory power of the

PD model in use did not deteriorate significantly from the moment of its

development. In order to test the discriminatory power of the PD model

in use, we will apply dp.testing function for the

PDtoolkit package.

#calculate again the AUC for the development sample

auc.dev <- auc.model(predictions = pd.db$pd, observed = pd.db$Creditability)

auc.dev## [1] 0.79465#test possible AUC deterioration on the application portfolio

dp.testing(app.port = app.port,

def.ind = "Creditability",

pdc = "pd",

auc.test = auc.dev,

alternative = "less",

alpha = 0.05)## auc auc.test estimate auc.se test.stat p.val alpha res

## 1 0.7821032 0.79465 -0.01254677 0.0247617 -0.5067005 0.3061825 0.05 H0: AUC >= AUC testSo, from the validation results, we can conclude that slight decrease

of AUC in application portfolio in comparison to development sample

cannot be considered as statistically significant for significance level

of 5%. Beside the discriminatory power, analysts are also interested in

testing the predictive ability of PD model in use. For this validation

procedure, hypothesis is that calibrated PDs are not underestimated,

i.e. they are not significantly lower than observed default rate.

Regarding the validation of model predictive power,

PDtoolkit package has pp.testing function.

Four tests are supported in this validation function: three of them

refer to testing on the rating grade level (binomial, Jeffreys,

z-score), while one refers to the complete rating scale (Hosmer-Lemeshow

test).

#summarise application portfolio to rating grade level

rs.ap <- app.port %>%

group_by(rating) %>%

summarise(no = n(),

nb = sum(Creditability),

ng = sum(1 - Creditability)) %>%

mutate(dr = nb / no)

#bring calibrated pd as a based for predictive power testing

rs.ap <- merge(rs[, c("rating", "pd")], rs.ap, by = "rating", all.x = TRUE)

rs.ap## rating pd no nb ng dr

## 1 01 (-Inf,473) 0.7400826 47 36 11 0.76595745

## 2 02 [473,482) 0.6069830 35 21 14 0.60000000

## 3 03 [482,506) 0.3750350 93 37 56 0.39784946

## 4 04 [506,515) 0.2516151 53 15 38 0.28301887

## 5 05 [515,547) 0.1537853 131 22 109 0.16793893

## 6 06 [547,Inf) 0.0500000 141 11 130 0.07801418#perform predictive power testing

pp.testing(rating.label = rs.ap$rating,

pdc = rs.ap$pd,

no = rs.ap$no,

nb = rs.ap$nb,

alpha = 0.05)## rating no nb odr pdc alpha binomial binomial.res jeffreys jeffreys.res zscore

## 1 01 (-Inf,473) 47 36 0.76595745 0.7400826 0.05 0.4159984 H0: ODR <= PDC 0.35159815 H0: ODR <= PDC 0.34293973

## 2 02 [473,482) 35 21 0.60000000 0.6069830 0.05 0.6059111 H0: ODR <= PDC 0.53854844 H0: ODR <= PDC 0.53370338

## 3 03 [482,506) 93 37 0.39784946 0.3750350 0.05 0.3613128 H0: ODR <= PDC 0.32231637 H0: ODR <= PDC 0.32475205

## 4 04 [506,515) 53 15 0.28301887 0.2516151 0.05 0.3479606 H0: ODR <= PDC 0.29276184 H0: ODR <= PDC 0.29914802

## 5 05 [515,547) 131 22 0.16793893 0.1537853 0.05 0.3621511 H0: ODR <= PDC 0.31876653 H0: ODR <= PDC 0.32669329

## 6 06 [547,Inf) 141 11 0.07801418 0.0500000 0.05 0.0966087 H0: ODR <= PDC 0.07085215 H0: ODR <= PDC 0.06346722

## zscore.res hosmer.lemeshow hosmer.lemeshow.res

## 1 H0: ODR <= PDC 0.7851538 H0: ODR <= PDC

## 2 H0: ODR <= PDC 0.7851538 H0: ODR <= PDC

## 3 H0: ODR <= PDC 0.7851538 H0: ODR <= PDC

## 4 H0: ODR <= PDC 0.7851538 H0: ODR <= PDC

## 5 H0: ODR <= PDC 0.7851538 H0: ODR <= PDC

## 6 H0: ODR <= PDC 0.7851538 H0: ODR <= PDCAs we can see from the results, all tests rejected the hypothesis of

underestimation of the calibrated PD in comparison to the observed

default rate. Sometimes the tests that serve the same purpose can

produce opposite results (lead to opposite conclusions) leaving analysts

in dilemma about overall conclusion. For that purpose we developed the

function power which implements simple framework of power

analysis of the statistical tests. More concretely, this function

calculates the power of the four tests used for predictive ability

testing. Assumption of the power analysis is that observed default rate

is the real default rate, so the ultimate goal of this analysis is to

quantify ability of each statistical test to detect the difference

between calibrated and real default rate.

power(rating.label = rs.ap$rating,

pdc = rs.ap$pd,

no = rs.ap$no,

nb = rs.ap$nb,

alpha = 0.05,

sim.num = 1000,

seed = 2211)## $interval.estimator

## rating no nb odr pdc binomial jeffreys zscore comment

## 1 01 (-Inf,473) 47 36 0.76595745 0.7400826 0.051 0.120 0.120 <NA>

## 2 02 [473,482) 35 21 0.60000000 0.6069830 NA NA NA ODR <= PDC

## 3 03 [482,506) 93 37 0.39784946 0.3750350 0.087 0.125 0.125 <NA>

## 4 04 [506,515) 53 15 0.28301887 0.2516151 0.088 0.142 0.142 <NA>

## 5 05 [515,547) 131 22 0.16793893 0.1537853 0.095 0.095 0.141 <NA>

## 6 06 [547,Inf) 141 11 0.07801418 0.0500000 0.287 0.391 0.391 <NA>

##

## $hosmer.lemeshow

## rating hosmer.lemeshow

## 1 01 (-Inf,473) + 02 [473,482) + 03 [482,506) + 04 [506,515) + 05 [515,547) + 06 [547,Inf) 0.268For this application portfolio characteristic we can conclude that in

average higher power of detecting the real underestimation of calibrated

PD have Jeffreys and z-score in comparison to the binomial test. Since

the Hosmer-Lemeshow test is the only test applied to the complete rating

scale, there is no other test to be compared with. For

additional package features that are implemented but not presented in

the above examples, please, check

help(package = "PDtoolkit").