![]()

![]()

The R package disaggR is an implementation of the French Quarterly National Accounts method for temporal disaggregation of time series. twoStepsBenchmark() and threeRuleSmooth() bend a time series with another one of a lower frequency.

You can install the stable version from CRAN.

You can install the development version from Github.

library(disaggR)

benchmark <- twoStepsBenchmark(hfserie = turnover,

lfserie = construction,

include.differenciation = TRUE)

as.ts(benchmark)

coef(benchmark)

summary(benchmark)

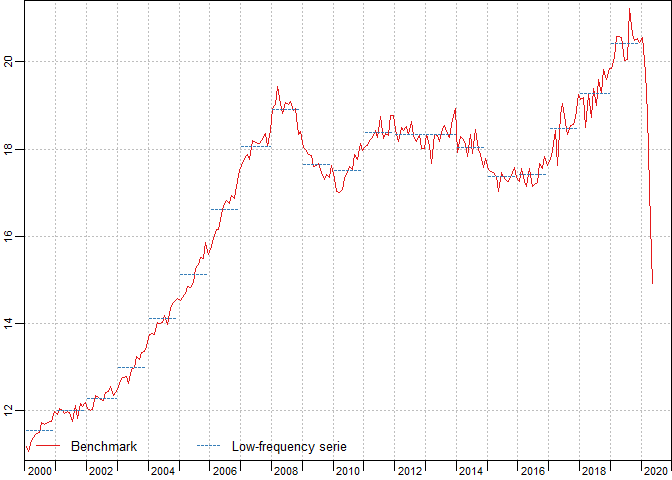

plot(benchmark)

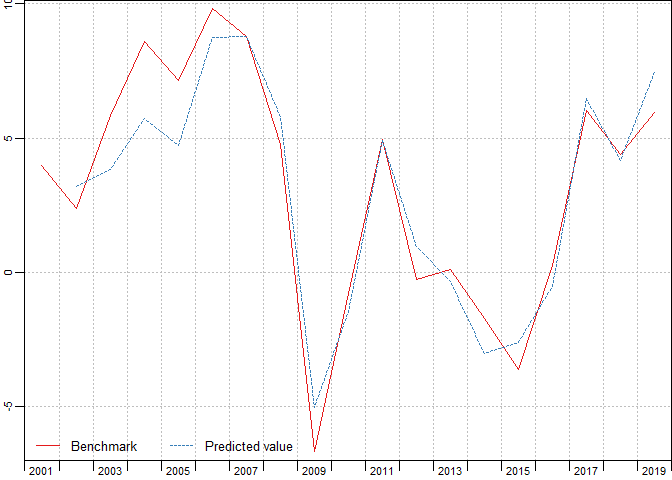

plot(in_sample(benchmark))

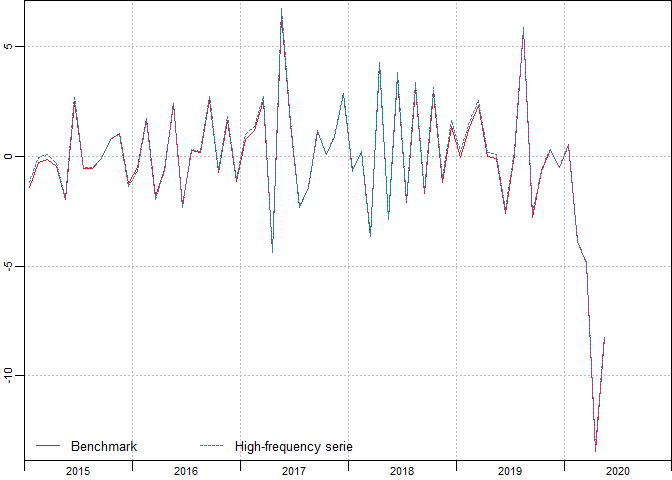

plot(in_disaggr(benchmark,type="changes"),

start=c(2015,1),end=c(2020,12))

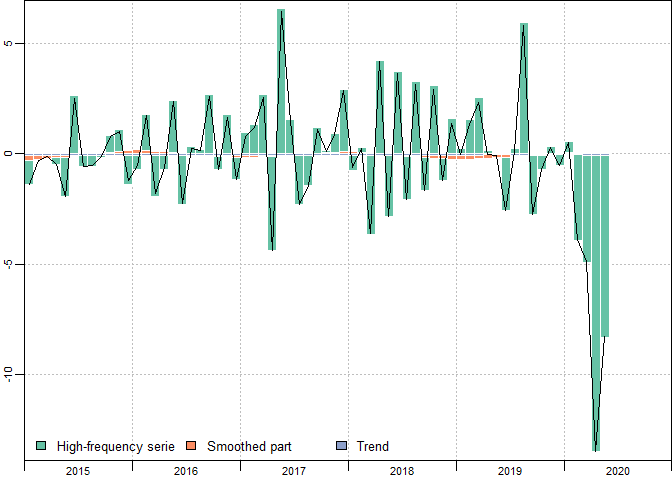

plot(in_disaggr(benchmark,type="contributions"),

start=c(2015,1),end=c(2020,12))

plot(in_scatter(benchmark))

new_benchmark <- twoStepsBenchmark(hfserie = turnover,

lfserie = construction,

include.differenciation = FALSE)

plot(in_revisions(new_benchmark,

benchmark),start = c(2010,1))

You can also use the shiny application reView, to easily chose the best parameters for your benchmark.