![]()

![]()

![]()

Get data from the Reserve Bank of Australia in a tidy tibble.

Install from CRAN using:

install.packages("readrba")Or install the development version from GitHub:

remotes::install_github("mattcowgill/readrba")library(ggplot2)

library(dplyr)

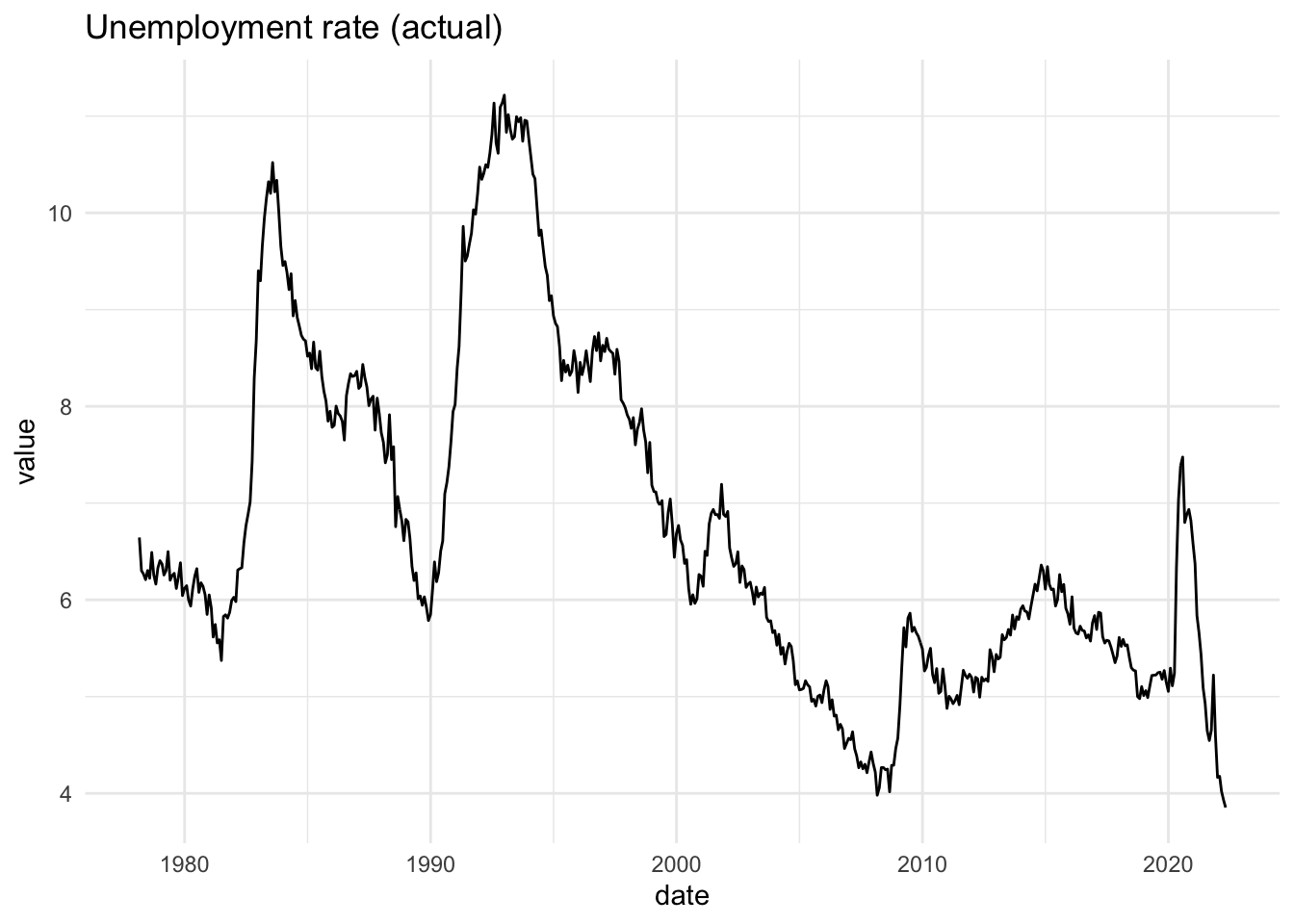

library(readrba)With a few lines of code, you can get a data series from the RBA and visualise it. Here’s the unemployment rate:

unemp_rate <- read_rba(series_id = "GLFSURSA")

unemp_rate %>%

ggplot(aes(x = date, y = value)) +

geom_line() +

theme_minimal() +

labs(title = "Unemployment rate (actual)")

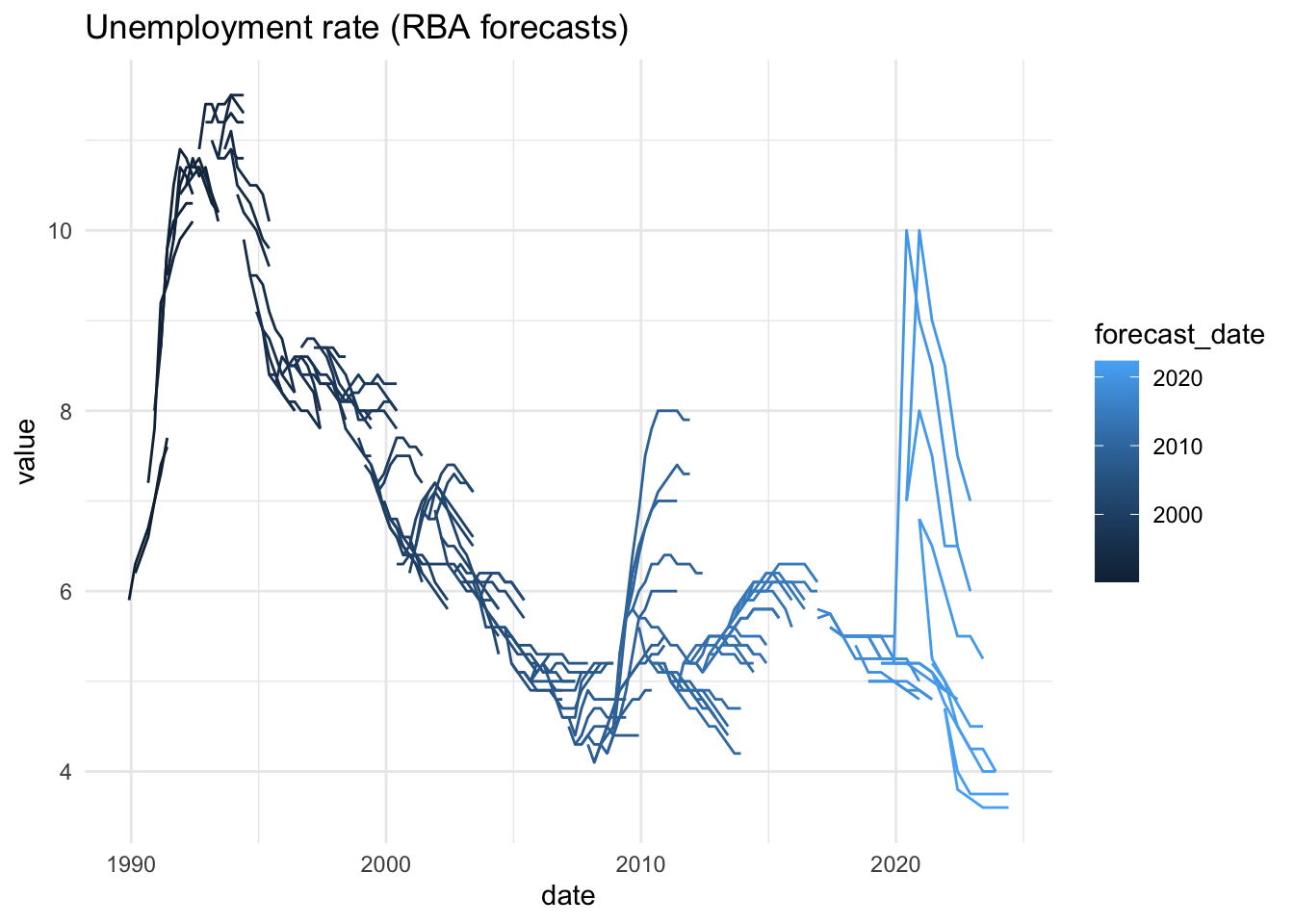

And you can also easily get the RBA’s public forecasts - from 1990 to present - and visualise those. Here’s every public forecast of the unemployment rate the RBA has made over the past three decades:

unemp_forecasts <- rba_forecasts() %>%

filter(series == "unemp_rate")

unemp_forecasts %>%

ggplot(aes(x = date,

y = value,

group = forecast_date,

col = forecast_date)) +

geom_line() +

theme_minimal() +

labs(title = "Unemployment rate (RBA forecasts)")

There primary function in {readrba} is read_rba().

Here’s how you fetch the current version of a single RBA statistical

table: table G1, consumer price inflation using

read_rba():

cpi_table <- read_rba(table_no = "g1")The object returned by read_rba() is a tidy tibble (ie.

in ‘long’ format):

head(cpi_table)

#> # A tibble: 6 × 11

#> date series value frequency series_type units source pub_date

#> <date> <chr> <dbl> <chr> <chr> <chr> <chr> <date>

#> 1 1922-06-01 Consumer price… 2.8 Quarterly Original Inde… ABS /… 2022-04-28

#> 2 1922-09-01 Consumer price… 2.8 Quarterly Original Inde… ABS /… 2022-04-28

#> 3 1922-12-01 Consumer price… 2.7 Quarterly Original Inde… ABS /… 2022-04-28

#> 4 1923-03-01 Consumer price… 2.7 Quarterly Original Inde… ABS /… 2022-04-28

#> 5 1923-06-01 Consumer price… 2.8 Quarterly Original Inde… ABS /… 2022-04-28

#> 6 1923-09-01 Consumer price… 2.9 Quarterly Original Inde… ABS /… 2022-04-28

#> # … with 3 more variables: series_id <chr>, description <chr>,

#> # table_title <chr>You can also request multiple tables. They’ll be returned together as one tidy tibble:

rba_data <- read_rba(table_no = c("a1", "g1"))

head(rba_data)

#> # A tibble: 6 × 11

#> date series value frequency series_type units source pub_date

#> <date> <chr> <dbl> <chr> <chr> <chr> <chr> <date>

#> 1 1994-06-01 Australian dol… 13680 Weekly Original $ mi… RBA 2022-06-10

#> 2 1994-06-08 Australian dol… 13055 Weekly Original $ mi… RBA 2022-06-10

#> 3 1994-06-15 Australian dol… 13086 Weekly Original $ mi… RBA 2022-06-10

#> 4 1994-06-22 Australian dol… 12802 Weekly Original $ mi… RBA 2022-06-10

#> 5 1994-06-29 Australian dol… 13563 Weekly Original $ mi… RBA 2022-06-10

#> 6 1994-07-06 Australian dol… 12179 Weekly Original $ mi… RBA 2022-06-10

#> # … with 3 more variables: series_id <chr>, description <chr>,

#> # table_title <chr>

unique(rba_data$table_title)

#> [1] "A1 Reserve Bank Of Australia - Liabilities And Assets - Summary"

#> [2] "G1 Consumer Price Inflation"You can also retrieve data based on the unique RBA time series identifier(s). For example, to getch the consumer price index series only:

cpi_series <- read_rba(series_id = "GCPIAG")

head(cpi_series)

#> # A tibble: 6 × 11

#> date series value frequency series_type units source pub_date

#> <date> <chr> <dbl> <chr> <chr> <chr> <chr> <date>

#> 1 1922-06-01 Consumer price… 2.8 Quarterly Original Inde… ABS /… 2022-04-28

#> 2 1922-09-01 Consumer price… 2.8 Quarterly Original Inde… ABS /… 2022-04-28

#> 3 1922-12-01 Consumer price… 2.7 Quarterly Original Inde… ABS /… 2022-04-28

#> 4 1923-03-01 Consumer price… 2.7 Quarterly Original Inde… ABS /… 2022-04-28

#> 5 1923-06-01 Consumer price… 2.8 Quarterly Original Inde… ABS /… 2022-04-28

#> 6 1923-09-01 Consumer price… 2.9 Quarterly Original Inde… ABS /… 2022-04-28

#> # … with 3 more variables: series_id <chr>, description <chr>,

#> # table_title <chr>

unique(cpi_series$series_id)

#> [1] "GCPIAG"The convenience function read_rba_seriesid() is a

wrapper around read_rba(). This means

read_rba_seriesid("GCPIAG") is equivalent to

read_rba(series_id = "GCPIAG").

By default, read_rba() fetches the current version of

whatever table you request. You can specify the historical version of a

table, if it’s available, using the cur_hist argument:

hist_a11 <- read_rba(table_no = "a1.1", cur_hist = "historical")

head(hist_a11)

#> # A tibble: 6 × 11

#> date series value frequency series_type units source pub_date

#> <date> <chr> <dbl> <chr> <chr> <chr> <chr> <date>

#> 1 1977-07-31 Australian Gov… 654 Monthly Original; … $ mi… RBA 2015-06-26

#> 2 1977-08-31 Australian Gov… 665 Monthly Original; … $ mi… RBA 2015-06-26

#> 3 1977-09-30 Australian Gov… 695 Monthly Original; … $ mi… RBA 2015-06-26

#> 4 1977-10-31 Australian Gov… 609 Monthly Original; … $ mi… RBA 2015-06-26

#> 5 1977-11-30 Australian Gov… 560 Monthly Original; … $ mi… RBA 2015-06-26

#> 6 1977-12-31 Australian Gov… 614 Monthly Original; … $ mi… RBA 2015-06-26

#> # … with 3 more variables: series_id <chr>, description <chr>,

#> # table_title <chr>Two functions are provided to help you find the table number or

series ID you need. These are browse_rba_tables() and

browse_rba_series(). Each returns a tibble with information

about the available RBA data.

browse_rba_tables()

#> # A tibble: 123 × 5

#> title no url current_or_hist… readable

#> <chr> <chr> <chr> <chr> <lgl>

#> 1 Liabilities and Assets – Summary A1 http… current TRUE

#> 2 Liabilities and Assets – Detailed A1.1 http… current TRUE

#> 3 Monetary Policy Changes A2 http… current TRUE

#> 4 Monetary Policy Operations – Current A3 http… current TRUE

#> 5 Holdings of Australian Government Secu… A3.1 http… current TRUE

#> 6 Securities Lending Repurchase and Swit… A3.2 http… current TRUE

#> 7 Foreign Exchange Transactions and Hold… A4 http… current TRUE

#> 8 Daily Foreign Exchange Market Interven… A5 http… current TRUE

#> 9 Banknotes on Issue by Denomination A6 http… current TRUE

#> 10 Detected Australian Counterfeits by De… A7 http… current TRUE

#> # … with 113 more rowsbrowse_rba_series()

#> # A tibble: 4,412 × 8

#> table_no series series_id series_type table_title cur_hist description

#> <chr> <chr> <chr> <chr> <chr> <chr> <chr>

#> 1 A1 Australian d… ARBAAASTW Original A1 Reserve… current Australian…

#> 2 A1 Capital and … ARBALCRFW Original A1 Reserve… current Capital an…

#> 3 A1 Deposits (ex… ARBALDEPW Original A1 Reserve… current Deposits (…

#> 4 A1 Exchange set… ARBALESBW Original A1 Reserve… current Exchange s…

#> 5 A1 Gold and for… ARBAAGFXW Original A1 Reserve… current Gold and f…

#> 6 A1 Notes on iss… ARBALNOIW Original A1 Reserve… current Notes on i…

#> 7 A1 Other assets… ARBAAOAW Original A1 Reserve… current Other asse…

#> 8 A1 Other liabil… ARBALOLW Original A1 Reserve… current Other liab…

#> 9 A1 Total assets ARBAATAW Original A1 Reserve… current Total RBA …

#> 10 A1 Total liabil… ARBALTLW Original A1 Reserve… current Total RBA …

#> # … with 4,402 more rows, and 1 more variable: frequency <chr>You can specify a search string to filter the tables or series, as in:

browse_rba_tables("inflation")

#> # A tibble: 3 × 5

#> title no url current_or_hist… readable

#> <chr> <chr> <chr> <chr> <lgl>

#> 1 Consumer Price Inflation G1 http… current TRUE

#> 2 Consumer Price Inflation – Expenditure … G2 http… current TRUE

#> 3 Inflation Expectations G3 http… current TRUEThe function rba_forecasts() provides easy access to all

the RBA’s public forecasts of key economic variables since 1990. The

function scrapes the RBA website to obtain the latest Statement on

Monetary Policy forecasts.

rba_forecasts()

#> # A tibble: 7,039 × 8

#> series_desc forecast_date notes source value date year_qtr series

#> <chr> <date> <chr> <chr> <dbl> <date> <dbl> <chr>

#> 1 CPI - 4 quarter … 1990-03-01 <NA> JEFG 8.6 1990-03-01 1990. cpi_a…

#> 2 CPI - 4 quarter … 1990-03-01 <NA> JEFG 7.6 1990-06-01 1990. cpi_a…

#> 3 CPI - 4 quarter … 1990-03-01 <NA> JEFG 6.5 1990-09-01 1990. cpi_a…

#> 4 CPI - 4 quarter … 1990-03-01 <NA> JEFG 6 1990-12-01 1990. cpi_a…

#> 5 CPI - 4 quarter … 1990-03-01 <NA> JEFG 5.9 1991-03-01 1991. cpi_a…

#> 6 CPI - 4 quarter … 1990-03-01 <NA> JEFG 6.2 1991-06-01 1991. cpi_a…

#> 7 Unemployment rat… 1990-03-01 <NA> JEFG 5.9 1989-12-01 1989. unemp…

#> 8 Unemployment rat… 1990-03-01 <NA> JEFG 6.3 1990-03-01 1990. unemp…

#> 9 Unemployment rat… 1990-03-01 <NA> JEFG 6.5 1990-06-01 1990. unemp…

#> 10 Unemployment rat… 1990-03-01 <NA> JEFG 6.7 1990-09-01 1990. unemp…

#> # … with 7,029 more rowsIf you just want the latest forecasts, you can request them:

rba_forecasts(all_or_latest = "latest")

#> # A tibble: 102 × 8

#> forecast_date date series value series_desc source notes year_qtr

#> <date> <date> <chr> <dbl> <chr> <chr> <chr> <dbl>

#> 1 2022-05-01 2021-12-01 aena_change 3.3 Nominal (n… SMP (a) … 2021.

#> 2 2022-05-01 2022-06-01 aena_change 6 Nominal (n… SMP (a) … 2022.

#> 3 2022-05-01 2022-12-01 aena_change 4.4 Nominal (n… SMP (a) … 2022.

#> 4 2022-05-01 2023-06-01 aena_change 4.8 Nominal (n… SMP (a) … 2023.

#> 5 2022-05-01 2023-12-01 aena_change 4.9 Nominal (n… SMP (a) … 2023.

#> 6 2022-05-01 2024-06-01 aena_change 4.9 Nominal (n… SMP (a) … 2024.

#> 7 2022-05-01 2021-12-01 business_in… 5.4 Business i… SMP (a) … 2021.

#> 8 2022-05-01 2022-06-01 business_in… -0.2 Business i… SMP (a) … 2022.

#> 9 2022-05-01 2022-12-01 business_in… 5 Business i… SMP (a) … 2022.

#> 10 2022-05-01 2023-06-01 business_in… 8.3 Business i… SMP (a) … 2023.

#> # … with 92 more rowsThe read_rba() function is able to import most tables on

the Statistical

Tables page of the RBA website. These are the tables that are

downloaded when you use read_rba(cur_hist = "current"), the

default.

read_rba() can also download many of the tables on the

Historical

Data page of the RBA website. To get these, specify

cur_hist = "historical" in read_rba().

The historical exchange rate tables do not have table numbers on the RBA website. They can still be downloaded, using the following table numbers:

| Table title | table_no |

|---|---|

| Exchange Rates – Daily – 1983 to 1986 | ex_daily_8386 |

| Exchange Rates – Daily – 1987 to 1990 | ex_daily_8790 |

| Exchange Rates – Daily – 1991 to 1994 | ex_daily_9194 |

| Exchange Rates – Daily – 1995 to 1998 | ex_daily_9598 |

| Exchange Rates – Daily – 1999 to 2002 | ex_daily_9902 |

| Exchange Rates – Daily – 2003 to 2006 | ex_daily_0306 |

| Exchange Rates – Daily – 2007 to 2009 | ex_daily_0709 |

| Exchange Rates – Daily – 2010 to 2013 | ex_daily_1013 |

| Exchange Rates – Daily – 2014 to 2017 | ex_daily_1417 |

| Exchange Rates – Daily – 2018 to Current | ex_daily_18cur |

| Exchange Rates – Monthly – January 2010 to latest complete month of current year | ex_monthly_10cur |

| Exchange Rates – Monthly – July 1969 to December 2009 | ex_monthly_6909 |

read_rba() is currently only able to import RBA

statistical tables that are formatted in a (more or less) standard way.

Some are formatted in a non-standard way, either because they’re

distributions rather than time series, or because they’re particularly

old.

Tables that are not able to be downloaded are:

| Table title | table_no | current_or_historical |

|---|---|---|

| Household Balance Sheets – Distribution | E3 | current |

| Household Gearing – Distribution | E4 | current |

| Household Financial Assets – Distribution | E5 | current |

| Household Non-Financial Assets – Distribution | E6 | current |

| Household Debt – Distribution | E7 | current |

| Open Market Operations – 2012 to 2013 | A3 | historical |

| Open Market Operations – 2009 to 2011 | A3 | historical |

| Open Market Operations – 2003 to 2008 | A3 | historical |

| Individual Banks’ Assets – 1991–1992 to 1997–1998 | J1 | historical |

| Individual Banks’ Liabilities – 1991–1992 to 1997–1998 | J2 | historical |

| Treasury Note Tenders - 1989–2006 | E4 | historical |

| Treasury Bond Tenders – 1982–2006 | E5 | historical |

| Treasury Bond Tenders – Amount Allotted, by Years to Maturity – 1982–2006 | E5 | historical |

| Treasury Bond Switch Tenders – 2008 | E6 | historical |

| Treasury Capital Indexed Bonds – 1985–2006 | E7 | historical |

I welcome any feature requests or bug reports. The best way is to file a GitHub issue.

I would welcome contributions to the package. Please start by filing an issue, outlining the bug you intend to fix or functionality you intend to add or modify.

This package is not affiliated with or endorsed by the Reserve Bank of Australia. All data is provided subject to any conditions and restrictions set out on the RBA website.